High Interest Rate and Inflation Challenges Create Financial Stress for a Segment of Vulnerable Canadian Borrowers

• In Q2 2022, TransUnion’s Credit Industry Indicator increased by 10 points year-on-year, after gains observed earlier in 2022

• A YoY improvement of ten points was driven by a slowing supply of credit, but was bolstered by increased balance and utilization activity, and continued improvement in credit performance

• Credit supply was affected by slowing origination volumes in mortgage and auto, driven by higher costs and affordability challenges

TransUnion today released the findings of its Canada Q2 2022 Credit Industry Insights Report (CIIR), which shows total debt grew to an all-time high at $2.24 trillion, up 9.2% year-over-year (YoY) and up 16.4% from pre-pandemic levels observed at the end of 2019. The number of consumers with a credit balance has increased by 2.1% YoY to 27.6 million and is up 2.5% from pre-pandemic levels (Q4 2019).

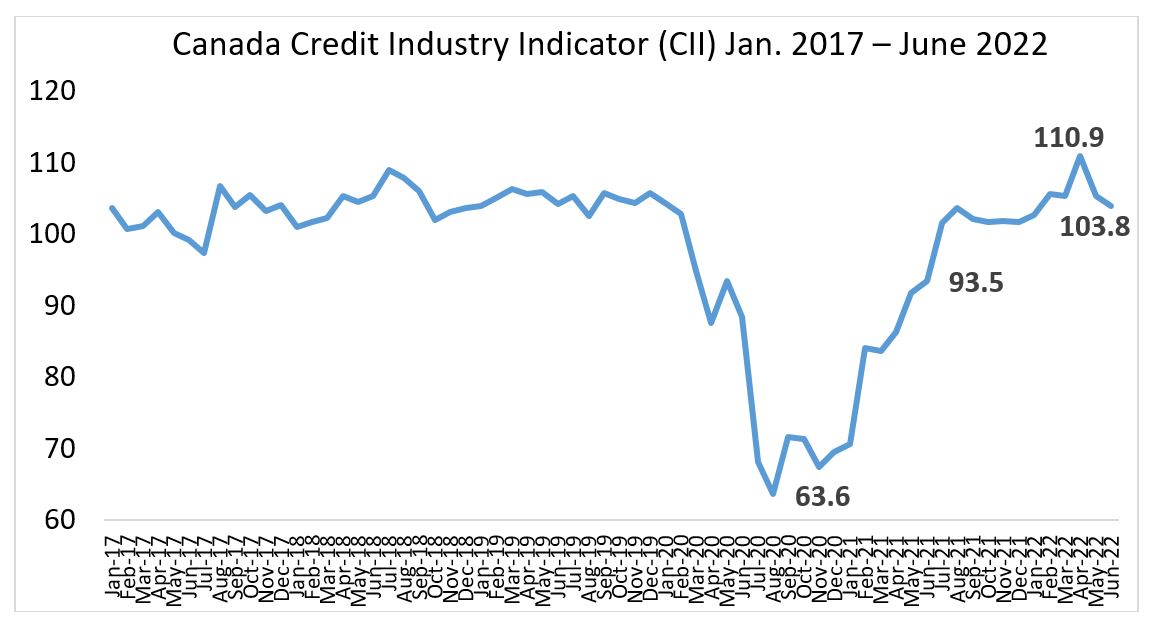

As part of the CIIR, TransUnion maps the consumer credit market health with its Credit Industry Indicator (CII), which rose 10 points YoY to 103.8 in June 2022, while falling seven points from the previous high in April 2022. The 12-month rise was driven by consumers and lenders re-engaging post-COVID-19, as well as recent increases in originations (a measure of new accounts opened) and balances. The CII fell toward the end of Q2 as a result of a slowing in supply of new credit provided by lenders, but was still bolstered by increased balance and utilization activity and continued improvement in credit performance.

These trends are likely to continue into the next quarter as Canadians face stronger economic headwinds in the coming months, particularly after the Bank of Canada raised its target interest rate by a full percentage point in July 2022 in an effort to fight inflation.

Chart 1: Canadian Credit Industry Indicator

Source: TransUnion Canada consumer credit database.

(i) A lower CII number compared to the prior period represents a decline in credit health, while a higher number reflects an improvement. The CII number needs to be looked at in relation to the previous period(s) and not in isolation. In June 2022, the CII of 103.8 represented an improvement in credit health compared to the same month prior year (June 2021) and a slight decline in credit health compared to the prior month (May 2022).

“With the combination of higher cost of living and higher spend driving up credit balances, along with the recent surge in mortgages and auto loans, many Canadian consumers are under pressure from higher debt service obligations,” said Matt Fabian, director of financial services research and consulting at TransUnion. “We’ve seen an increase in miminum payment amounts of up to 10% in the first half of 2022, depending on the combination of products consumers hold, along with a slight deterioration in payment behaviours.”

Increased balance growth was observed across all risk tiers, with super prime consumers continuing to build overall outstanding balances (+5.1% YoY). The number of subprime consumers with a credit balance grew by 4.8% YoY in Q2, marking a shift in risk appetite by lenders towards higher risk borrowers compared to the pandemic lows. This is potentially caused by higher consumer demand to cope with the effects of inflation and increasing interest rates. All major credit products saw an increase in average balance per borrower, indicating the consumer need to leverage credit.

Table 1: Balance Growth by Product

| Average balance per consumer | Q2 2021 | Q2 2022 | YoY % change |

| Credit Cards | $ 3,448 | $ 3,825 | 10.9% |

| Personal Loans | $ 47,144 | $ 56,723 | 20.3% |

| Auto Loans | $ 24,726 | $ 25,539 | 3.3% |

| Lines of Credit | $ 33,447 | $ 34,697 | 3.7% |

| Mortgages | $ 304,772 | $ 333,788 | 9.5% |

“During the pandemic we saw a decline in credit participation among below prime consumers, so this marks a re-engagement of this segment as potentially the effects of inflation and interest rates have driven demand, while lenders have increased their risk appetite in this space,” Fabian adds.

Overall, consumer-level delinquencies (borrowers more than 90 days past due on any account) increased by four basis points (bps) over the prior year same quarter, but still remain below pre-pandemic levels. Consumer delinquency on personal loans has returned to pre-pandemic levels, up 19 bps YoY, to 0.93%. Credit card delinquency (90 days or more past due) is also higher by six bps from the prior year same quarter. The increase in consumer delinquencies is partially explained by accelerated lender origination activity, especially in the below prime space. The YoY rises in delinquencies are generally small and not a major concern, given the increased credit activity observed post pandemic. As credit activity recovers and grows further, consumer credit performance is expected to return to near pre-pandemic levels.

Core macro-economic indicators remain strong, but payment shock is concerning

Coming out of the pandemic, core macroeconomic indicators remain strong in terms of GDP growth and low unemployment[1]; however, these gains have been offset by higher interest rates and cost of living. While the average annual wage increase in some sectors was as high as 9.3%[2], increases in inflation and interest rates eroded disposable income and savings rates. Despite increasing wages, consumers’ salaries have not kept up with fast-rising inflation.[3]

“The implications of interest rate hikes and rising inflation are significant, with the heightened cost of living that leads to higher credit balances as consumers borrow to fund day-to-day expenses. This combined with increased debt service levels for mortgages, auto and personal loans are all creating a rapid increase in payment obligations beyond consumers’ control,” says Fabian. “A proportion of vulnerable consumers who do not have the capacity to meet these increased payments may face the additional impacts of the current interest rate environment escalating before it recedes, setting them up for a sustained period of payment shock.”

TransUnion’s Q2 2022 Consumer Pulse Survey found 41% of consumers reported that their household finances were worse than planned (up 5% from prior year), with 48% reporting they had cut back on discretionary spending. Over a quarter (26%) of consumers expect to be unable to repay their bills and loans.

Furthermore, 63% said that they are very or extremely concerned about the current rate of inflation, with 68% making changes to their purchasing behaviour because of the current high inflation environment. 27% of Canadians decided not to apply for credit, as the cost of new credit or refinancing was too high.

This is in a context of inflation at a 30-year high, energy prices having increased by 36.4%, food inflation being at a 20-year high, and shelter costs remaining elevated.[4]

A recent research study from TransUnion looked at consumers’ capacity to absorb increased monthly payments due to interest rate increases as well as the impact of inflation on discretionary income. The research used trended data to assess consumers’ available cash flow based on how much they are paying each month above the minimum due amounts on their debt obligations, and simulated several interest rate and inflation scenarios to observe how these events impacted the payment amount.

The study found that as many as 7.8 million Canadian consumers might have a negative capacity to absorb a $200 monthly increase in cost of living based on their current payment behaviours, and may be unable to keep up with their credit obligations. If the cost of living increased by $500 monthly, as many as 9.6 million consumers would be impacted.

Additionally, as many as 1.5 million Canadian consumers could be impacted by a payment shock arising from a 150 basis point interest rate increase because these consumers carry variable rate products such as variable rate mortgages and lines of credit in their wallets. As interest rates rise, the minimum payment due is bound to increase and for consumers who are unable to meet their payment obligations due to this shock are expected to be impacted.

While inflation and interest rates are correlated they are not necessarily mutually exclusive. Some consumers are impacted in a dual shock scenario where cost of living decreases their disposable income allocation while at the same time the debt costs are increasing. Overlaying consumers impacted by a $200 monthly cost increase due to inflation and those also impacted by a 100 bps interest rate increases, about 1.3 million consumers are revealed to have a negative capacity to absorb both.

This does not necessarily indicate that these consumers will default on debt payments and become delinquent or insolvent – but it does mean that they will have to make trade-offs in how they spend any discretionary income that they have, and how this is allocated to debt and other expenses. Additionally, there is a segment of consumers that will use existing cash flow to cover credit obligations and potentially either forego other non-credit items or perhaps look for additional credit access to offset short-term liquidity.

“Mitigating risk in existing portfolios becomes a priority in the current environment to help reduce future losses. Success is dependent on multiple factors: monitoring processes and frequency, using robust data sets to assess risk, and executing differentiated treatment strategies,” Fabian said. “While many consumers have been impacted by the current high interest rate and high inflation environment, most have the capacity to absorb payment shocks. Attracting and acquiring the consumers that are resilient to payment shocks is the key to solving for prudent growth in the near future.”

For more information about the Q2 2022 Credit Industry Insights Report, please click here.

About TransUnion (NYSE: TRU)

TransUnion is a global information and insights company that makes trust possible in the modern economy. We do this by providing an actionable picture of each person so they can be reliably represented in the marketplace. As a result, businesses and consumers can transact with confidence and achieve great things. We call this Information for Good® TransUnion provides solutions that help create economic opportunity, great experiences and personal empowerment for hundreds of millions of people in more than 30 countries. Our customers in Canada comprise some of the nation’s largest banks and card issuers, and TransUnion is a major credit reporting, fraud, and analytics solutions provider across the finance, retail, telecommunications, utilities, government and insurance sectors.

For more information or to request an interview, contact:

Contact Emma Tiessen

E-mail Emma.Tiessen@ketchum.com

Telephone 647-523-1594

[1] GDP annual growth rate is 2.9%, unemployment rate is 4.9% - Canada Indicators (tradingeconomics.com)

[2] Canada Average Weekly Earnings YoY - July 2022 Data - 1992-2021 Historical (tradingeconomics.com)

[3] Source: Oxford Economics, Statistics Canada. Table 14-10-0064-01 Employee wages by industry, annual

[4] Source: Oxford Economics, Statistics Canada. Table 14-10-0064-01 Employee wages by industry, annual